If you work for a private employer that provides employee benefits, you may have access to a 401(k) plan to help you save for retirement. If you’re a federal government employee, you’re offered the Thrift Savings Plan (TSP), a similar program where you can also contribute a portion of your earnings to invest towards retirement. If you’re a business owner looking to save for retirement in a tax-efficient manner, click here to read our retirement planning tips for business owners.

A 401(k) or Thrift Savings Plan (TSP) offers a powerful way to save for the future, but many people struggle with one critical question: How much should I contribute to my 401(k) or TSP to ensure I’m ready for retirement?

In this guide, we’ll break down the contribution limits for both 401(k)s and TSPs and help you craft a personalized contribution strategy. By the end, you’ll be equipped to optimize your savings and stay on track to achieve your ideal retirement lifestyle.

What Is a 401(k) or TSP Account? And Why Contribute?

A 401(k) is a retirement savings plan offered by private employers, allowing you to set aside a portion of your pre-tax income to save for your future.

Similarly, the Thrift Savings Plan (TSP) is a retirement plan designed specifically for federal employees and members of the uniformed services.

So why should you take a portion of your salary each month to make regular 401(k) or TSP contributions? Contributing to these plans may allow you to:

- Lower your taxable income (with traditional contributions)

- Take advantage of compounding growth over time

- Build a financial cushion for a comfortable retirement

Both 401(k) and TSP plans offer significant benefits, including tax-deferred growth on your investments, and many employers or agencies provide matching contributions, which is essentially free money toward your retirement savings.

One of the most powerful features of these accounts is that you can invest the money you contribute, potentially growing your savings over time.

401(k) and TSP Contribution Limits 2025: How Much CAN You Contribute?

The federal government places a cap on how much you can contribute to your 401(k) or TSP each year. These limits are in place to encourage retirement savings while also ensuring that these tax-advantaged accounts are not disproportionately used by high-income earners to defer taxes.

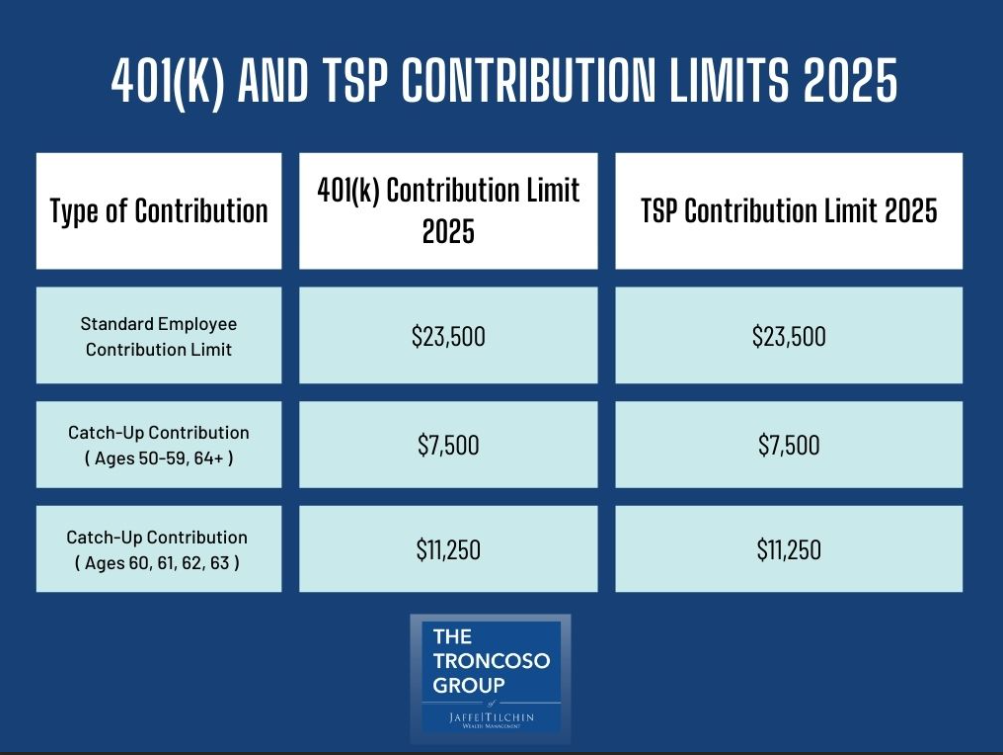

For 2025, the IRS has set the following 401(k) and TSP contribution limits:

To view the latest contribution limits and IRA contribution limits, click here to visit the IRS.gov website.

Maximizing your contributions within these limits is a critical step in building a robust retirement fund. If you’re unable to reach the full limit, contributing as much as you can—even if it’s a smaller amount—ensures you’re making the most of your retirement plan. For those eligible for an employer match, it’s especially important to contribute enough to take advantage of this additional “free money.”

Employer Match: “Free Money” That Helps You Grow Your Retirement Assets Even Further

An employer match is a powerful benefit offered by many 401(k) and TSP plans, where your employer contributes additional money to your retirement account based on how much you contribute.

For example, an employer might match 100% of your contributions up to 4% of your salary. This is essentially free money that boosts your retirement savings, making it important to contribute enough to at least maximize your employer’s match.

Failing to do so is like leaving money on the table, so take full advantage of this benefit if it’s available.

Understanding the Tax Benefits of 401(k) Contributions

One of the greatest advantages of 401(k) and TSP plans is their tax benefits. Contributions to a traditional 401(k) or TSP are made with pre-tax dollars, reducing your taxable income for the year. Alternatively, Roth 401(k) or Roth TSP contributions are made with after-tax dollars but allow for tax-free withdrawals in retirement.

Does Your 401(k) Contribution Reduce Taxable Income?

Yes, contributions to a traditional 401(k) or traditional TSP are tax-deductible, meaning they lower your taxable income. For example, if you earn $60,000 annually and contribute $10,000 to your 401(k), you’ll only pay taxes on $50,000. This immediate tax benefit makes 401(k) plans an attractive option for many savers.

Additionally, the funds in your account grow tax-deferred. This means you won’t pay taxes on any investment gains, dividends, or interest earned while your money remains in the account. Taxes are only due when you withdraw the funds during retirement, at which point these withdrawals will be taxed as ordinary income.

Roth vs. Traditional 401(k) or TSP

While traditional 401(k) or TSP plans offer immediate tax savings, Roth 401(k) or TSP plans provide tax-free income in retirement. Deciding which option is best for you depends on factors like your current income level, anticipated retirement income, and tax rates. Many employers now offer the flexibility to split contributions between traditional and Roth accounts.

If you opt for a Roth 401(k) or Roth TSP option, the tax benefits work a little differently. Contributions are made with after-tax dollars, meaning you don’t get an immediate tax deduction.

However, the major advantage is that your investment growth and withdrawals during retirement are entirely tax-free, as long as you meet the withdrawal requirements. This can be a powerful strategy for those who anticipate being in a higher tax bracket in retirement or want to reduce their taxable income later in life.

How Much Should You Contribute to Your 401(k)?

Determining the right 401(k) or TSP contribution amount depends on your financial goals, retirement timeline, and current circumstances. Here are some general guidelines:

- Contribute at Least Enough to Take Advantage of the Employer Match

Employer matching is a key factor in your contribution decision. For instance, if your employer offers a 100% match on contributions up to 5% of your salary, you should contribute at least 5% to maximize this benefit. Not doing so is leaving money on the table that could significantly boost your retirement savings.

- Use the 15% Rule

Many financial experts recommend contributing 15% of your salary, including employer matches, toward retirement savings. For example, if your employer matches 5%, you would need to contribute 10% to reach the recommended total. This rule ensures you’re saving enough to build a robust nest egg for the future.

- Try the 50/30/20 Rule

This budgeting rule can also guide your retirement contributions. Allocate:

- 50% of your income to necessities (housing, food, utilities)

- 30% to discretionary spending

- 20% to savings, which can include your 401(k)

By following this framework, you can balance your immediate financial needs with your long-term savings goals.

Because everyone’s financial and retirement planning goals are different, it’s also a good idea to consult with a financial planner to help you project your retirement needs and the amount you should be saving each year to achieve those goals.

So is there a quick way to answer the question of how much should you contribute to 401(k) or TSP retirement plans based on how much money you think you’ll need to live on in retirement?

The quick rule of thumb that can be used as an initial guide is the 4% rule that we’ll take a look at below.

Estimate Your Retirement Savings Goals with the 4% Rule

Based on years of financial planning research, the 4% rule assumes that you can safely withdraw 4% of your savings each year during retirement without depleting your funds for at least 30 years.

To calculate your retirement goal using this rule of thumb, start by determining how much income you’ll need annually in retirement. Then, multiply that number by 25.

For example, if you aim to have $60,000 per year to cover living expenses, you would need approximately $1.5 million in savings ($60,000 x 25).

Keep in mind that this rule is a general guideline. It assumes a diversified portfolio of stocks and bonds and doesn’t factor in taxes, inflation, or potential changes in spending habits.

However, it’s a good starting point to assess your long-term savings needs. From there, you can refine your goal by considering variables like healthcare costs, your desired retirement age, and other sources of income such as Social Security or pensions.

3 Factors That Influence Your 401(k) or TSP Contribution Rate

- Age and Retirement Timeline

Consistency and time are your greatest allies in building a substantial retirement fund. The earlier you start contributing to your 401(k) or TSP, the more time your money has to grow through the power of compounding interest.

Let’s look at an example of someone contributing $1,000 per month to their 401(k), assuming a 7% annual return, and compare the outcomes based on the age they start contributing:

- Starting a 401(k) at 25:

By the time you reach 65, you’ll have contributed $480,000 over 40 years. However, thanks to compounding, your account could grow to $2.44 million. - Starting a 401(k) at 30:

Contributing $1,000 per month for 35 years results in $420,000 in contributions. With compounding, your account could grow to $1.85 million by age 65. - Starting a 401(k) at 35:

Over 30 years, you’ll contribute $360,000. With the same growth rate, your account could grow to $1.37 million by retirement.

This example highlights the importance of starting early. Those extra years allow your money to compound significantly, resulting in much larger retirement savings.

While it’s never too late to start contributing to your 401(k) or TSP, you may need to contribute more aggressively to make up for lost time.

- Using Your Catch-Up Contribution Opportunities

For those aged 50 and older, catch-up contributions provide an excellent opportunity to save more for retirement. In 2025, the 401(k) and TSP catch-up contribution limit for those between ages 50 and 59 and 64+ is $7,500.

Starting in 2025, those between ages 60-63 can now make an even larger catch-up contribution of $11,250. These numbers are in addition to the regular $23,500 contribution limit for 2025.

For example, if you’re 61 years old and maximizing both your regular and catch-up contributions in 2025, you could save up to $34,750 in your 401(k) or TSP for the year. These extra contributions, when paired with potential employer matching and investment growth, can significantly boost your retirement nest egg.

- Income and Budget Considerations

Your current financial situation will also influence your contribution rate. Start with what you can afford and gradually increase your contributions over time—for example, by 1% each year or whenever you receive a raise. This incremental approach allows you to prioritize retirement without feeling an immediate financial strain.

How Can You Invest Your 401(k) or TSP Contributions?

The growth you experience in your 401(k) or TSP account will depend on the types of assets you invest in. While every 401(k) plan offers different investment options, you will generally have access to several asset classes that allow you to have a diversified portfolio to save towards your retirement.

A TSP may offer more limited options, allowing you to invest in just a few of the major asset classes until you eventually roll it over into an IRA once you retire. Click here to read more about TSP investment options.

Here’s a brief overview of the main asset classes you can likely invest in with your 401(k) or TSP contribution money:

- Stocks: Often considered the engine of growth in your portfolio, stocks represent ownership in companies and can deliver strong returns over the long term. However, they tend to be more volatile, which means their value can fluctuate significantly in the short term.

- Bonds: Bonds are debt securities issued by governments or corporations. They typically provide more stable returns than stocks and can serve as a counterbalance in your portfolio. While they tend to grow more slowly, bonds are generally less volatile.

- Cash and Cash Equivalents: These include money market funds or stable value funds, which offer low risk but also lower returns. These are ideal for preserving capital or for those nearing retirement who want to reduce market exposure.

- Lifecycle or target-date funds: Both 401(k)s and TSPs often offer lifecycle or target-date funds that automatically adjust your asset allocation as you approach retirement.

By strategically investing your money across these asset classes, you can take advantage of the compounding growth of your contributions. If you’re unsure how to invest your contributions, it may be a good idea to chat about your retirement planning goals with a financial planner so you can align your investment strategy with your goals, risk tolerance, and timeline.

Actionable Tips for Optimizing Your 401(k) Contributions

Contributing to a 401(k) or TSP is one of the smartest ways to prepare for retirement, but determining the right contribution amount requires careful consideration of your age, income, and financial goals. Here some key tips to remember:

- Automate Your Contributions: Set up automatic payroll deductions to ensure consistency and eliminate the risk of forgetting to contribute.

- Increase Contributions Over Time: Aim to raise your contribution rate annually or with each salary increase. Even small increases can have a significant impact over the long term.

- Maximize Employer Match: Always contribute enough to get the full employer match. It’s one of the easiest ways to boost your savings without additional effort.

- Diversify Your Investments: Ensure your 401(k) portfolio is diversified to balance risk and return based on your age and risk tolerance.

- Seek Professional Advice: Consult a financial advisor to tailor your retirement savings strategy to your unique goals and circumstances. An expert can help you navigate complex decisions, such as balancing debt repayment with retirement contributions.

By starting early, maximizing employer matches, and taking advantage of tax benefits, you can set yourself up for a secure and comfortable retirement. Remember, every dollar you contribute today brings you closer to financial independence.

Want professional guidance in taking the next step in your retirement planning? Learn about our retirement planning services here or schedule an initial chat with one of our financial advisors in Tampa today.